Most investors watch the stock market for signs of trouble. When equity indices fall, panic begins. But in many cases, the first warning signs do not appear in the stock market. They appear quietly in the credit market.

Credit markets include corporate bonds, bank loans, government bonds, private credit, and other forms of borrowing and lending. In simple words, this is the place where companies, governments, and institutions borrow money.

When lenders become nervous, borrowers start facing pressure. Interest costs rise, refinancing becomes difficult, defaults increase, and weaker companies begin to struggle. These signals often appear before the broader economy shows visible signs of slowdown.

That is why understanding credit market warning signs can help investors become more aware, more disciplined, and less reactive.

What Are Credit Markets?

Credit markets are financial markets where borrowers raise money and lenders provide capital. A company may issue bonds to fund expansion. A government may borrow to finance spending. A bank may give loans to businesses. Private credit funds may lend directly to companies.

The credit market tells us one important thing: how confident lenders are about getting their money back.

When confidence is strong, borrowers can raise money easily at lower rates. When confidence weakens, lenders demand higher returns, impose stricter conditions, or stop lending to riskier borrowers.

This change in lending behaviour is one of the earliest signs of stress in the financial system.

Why Credit Markets Matter Before a Downturn?

A downturn usually does not begin suddenly. It builds slowly through pressure points.

Companies may first face higher borrowing costs. Then their profit margins may shrink. After that, they may cut spending, delay expansion, reduce hiring, or restructure debt. Eventually, defaults may rise.

The IMF’s April 2026 Global Financial Stability Report noted that financial stability risks remain elevated, with concerns around high debt levels, rollover risks, leverage in non-bank financial institutions, and interconnectedness across markets.

This means credit markets are not just a technical subject for bond investors. They are an important economic signal for equity investors, mutual fund investors, business owners, and policymakers.

1. Credit Spreads: The First Warning Signal

One of the most important indicators in credit markets is the credit spread.

A credit spread is the extra return investors demand for lending to a company instead of lending to a safer government borrower. For example, if a government bond gives 6% and a corporate bond gives 8%, the spread is 2%.

When investors feel safe, credit spreads remain low. When they become worried, spreads widen.

Simple Meaning : A rising credit spread means lenders are asking for more compensation because they see higher risk.

Why It Matters?

If spreads rise sharply, companies may find it more expensive to borrow. This affects profitability, expansion, hiring, and debt repayment ability.

The OECD’s 2026 Global Debt Report noted that corporate credit spreads were near historical lows even for riskier borrowers, despite macroeconomic and geopolitical uncertainty. It also highlighted record corporate borrowing in 2025 and growing capital needs linked to AI expansion.

This type of situation can be important because very low spreads may show investor confidence, but they may also show that markets are underpricing future risk.

2. Rising Default Rates

A default happens when a borrower fails to make interest or principal payments on time.

Defaults usually rise when companies face weak earnings, high debt, poor cash flow, or difficulty refinancing loans.

Moody’s Analytics reported in April 2026 that its baseline forecast expected default rates to decline through 2026 after a temporary spike in the first quarter. However, Moody’s also noted that default forecasts remain vulnerable to credit shocks.

What Investors Should Watch?

Investors should not only look at the headline default rate. They should also watch:

A sudden rise in defaults can be a strong signal that the credit cycle is turning.

3. Refinancing Pressure

Many companies do not repay all debt from cash flow. They refinance old debt by raising new debt.

This works smoothly when interest rates are low and lenders are confident. But when interest rates rise or market conditions tighten, refinancing becomes difficult.

Simple Example:

Suppose a company borrowed at 6% five years ago. Now that loan is maturing, and the company has to refinance at 10%. Even if the company’s sales are stable, its interest cost rises sharply.

This can reduce profit and weaken its ability to invest, expand, or repay future debt.

Why It Becomes Dangerous?

Refinancing pressure becomes serious when many companies need to repay or renew debt at the same time. If lenders become cautious, weaker companies may not get fresh funding easily.

This is why the IMF has highlighted rollover risk as a financial stability concern.

4. Private Credit: The Less Visible Risk

Private credit has grown rapidly in recent years. It involves lending by non-bank institutions, often directly to companies.

Private credit can be useful because it provides funding outside traditional banks. But it can also create risks because it is less transparent than public bond markets.

In May 2026, the Financial Stability Board warned about rising links between banks, asset managers, insurers, and private credit markets. Reuters reported that the private credit market is estimated at around $1.5 trillion to $2 trillion, with some measures going up to $3.5 trillion, and that regulators are concerned about opacity, leverage, liquidity mismatch, and rising retail participation.

Why Investors Should Care?

Private credit problems may not appear immediately in public markets. But stress can spread through banks, insurers, funds, and asset managers if losses rise.

The risk is not only about one borrower failing. The larger concern is interconnectedness.

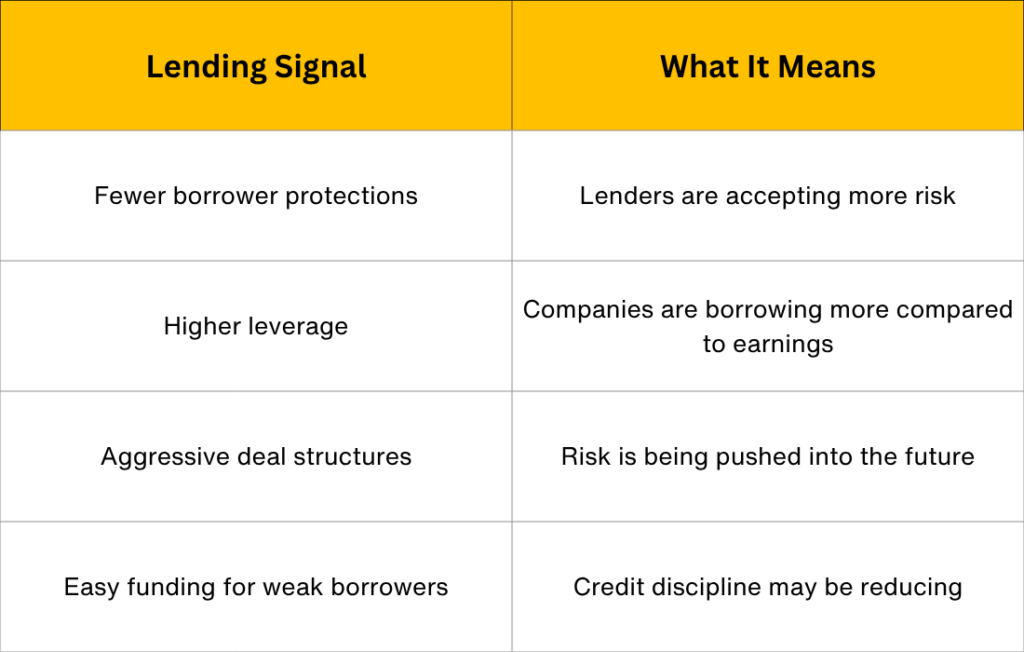

5. Weakening Lending Standards.

During strong market phases, lenders often compete to give loans. This can lead to relaxed lending conditions.

Some warning signs include:

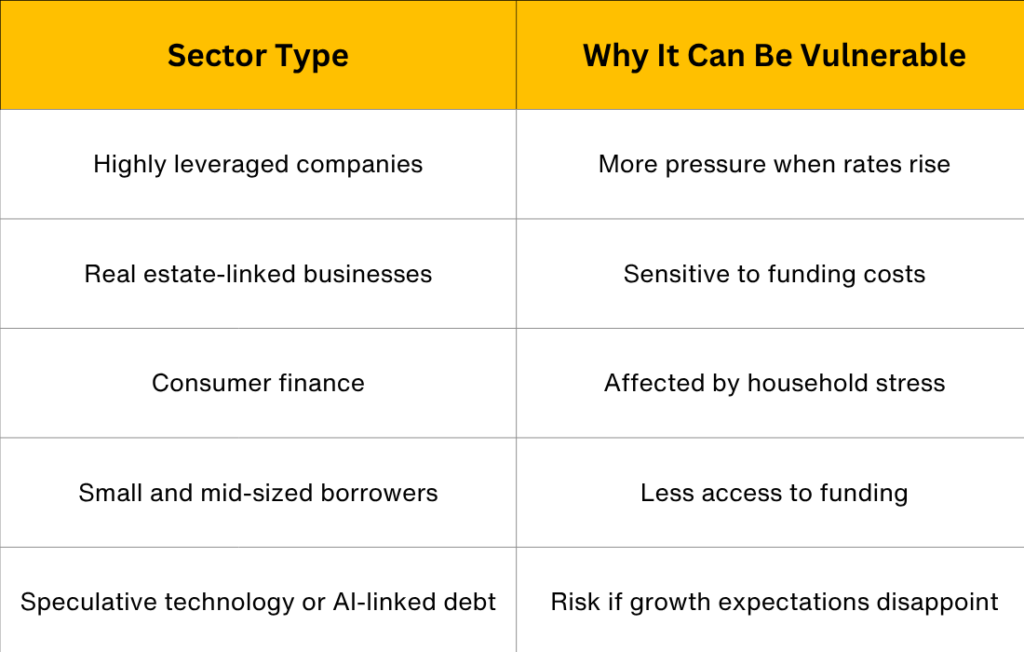

6. Sector-Specific Stress.

Credit stress does not always begin across the whole economy. It often starts in specific sectors.

For example, sectors with high debt, weak demand, high input costs, or sensitivity to interest rates may show early trouble.

Investors should watch sectors such as:

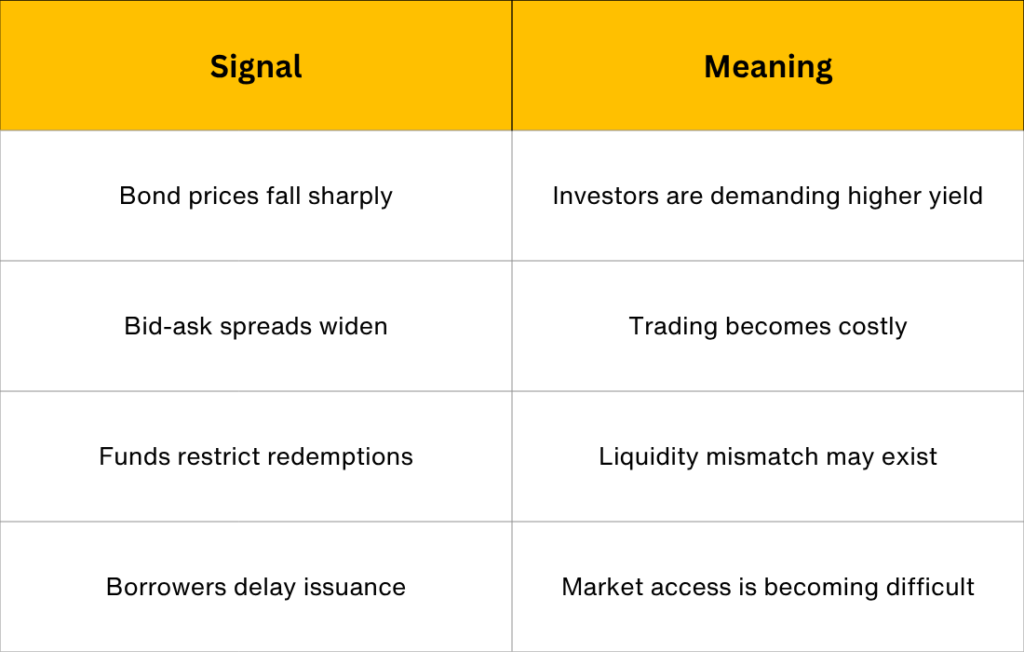

7. Liquidity Stress

Liquidity means the ability to buy, sell, borrow, or repay without major disruption.

In normal markets, liquidity looks strong. But during stress, buyers disappear, borrowing costs rise, and selling assets becomes difficult.

Warning Signs of Liquidity Stress:

Liquidity stress can turn a manageable problem into a serious downturn because companies may not get funding when they need it most.

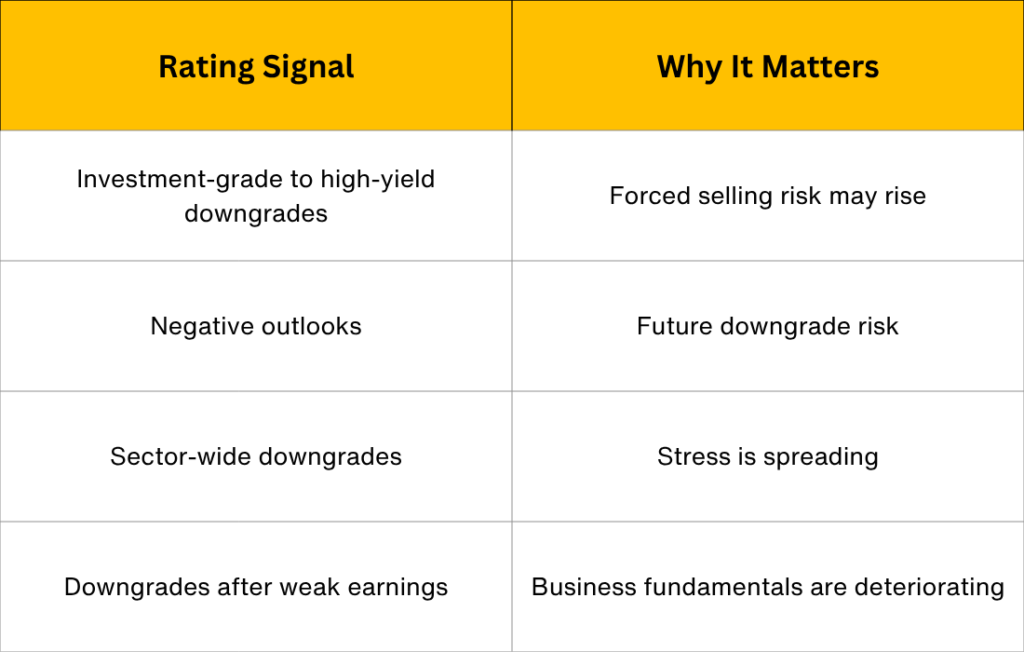

8. Rating Downgrades.

Credit rating agencies evaluate the repayment ability of borrowers. A downgrade means the borrower’s credit quality has weakened.

One downgrade may not be a crisis. But a wave of downgrades can indicate deeper market stress.

Important Rating Signals:

Investors should watch:

When many companies move closer to lower-rated categories, the credit market becomes more fragile.

9. Yield Curve and Bond Market Signals.

The bond market can also give early signals about economic expectations.

A steep rise in yields may show inflation or fiscal concerns. A fall in long-term yields may show growth fears. An inverted yield curve can indicate expectations of future slowdown.

But investors should not depend on one signal alone. Credit spreads, defaults, refinancing risk, liquidity, and earnings trends should be studied together.

10. What Equity and Mutual Fund Investors Can Learn.

Credit market stress can affect equity markets because companies depend on funding.

When credit becomes expensive:

• Companies may reduce expansion.

• Profit margins may weaken.

• Highly indebted companies may underperform.

• Banks and financial companies may become cautious.

• Market sentiment may turn risk-off.

For mutual fund investors, this does not mean panic selling. It means investors should understand the quality of the funds they hold, their time horizon, and the risk level of underlying assets.

Debt fund investors should especially understand credit quality, duration risk, liquidity risk, and portfolio concentration.

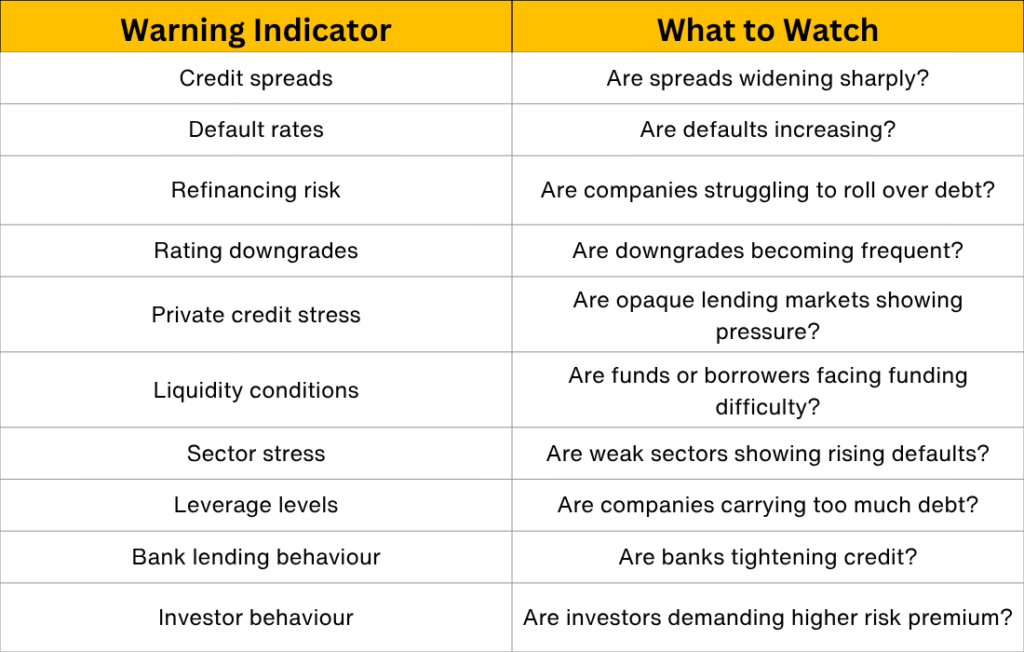

Early Warning Checklist for Investors:

Here is a simple checklist investors can follow:

This checklist can help investors read the market more calmly instead of reacting only after headlines become negative.

Real-Life Example: Why Credit Stress Matters

Imagine a company that borrowed heavily when interest rates were low. Its business looked strong because borrowing was cheap.

Now interest rates rise. The company’s old loan matures. It must refinance at a much higher rate. At the same time, demand slows and profits fall.

The company now has three problems:

• Higher interest cost.

• Lower profit.

• Difficulty raising fresh money.

If many companies face this situation together, the credit market starts showing stress. Eventually, this can affect jobs, investment, consumption, and stock market performance.

This is why credit markets are often called the economy’s early warning system.

How Investors Should Respond?

Credit market warning signs are not a reason to panic. They are a reason to review.

Investors can consider:

• Avoiding excessive concentration in risky assets.

• Reviewing debt fund portfolio quality.

• Maintaining emergency liquidity.

• Staying disciplined with long-term SIPs.

• Avoiding decisions based only on short-term market noise.

• Understanding risk before chasing higher returns.

• Taking professional guidance where needed.

The goal is not to predict the exact next downturn. The goal is to avoid being surprised by it.

Conclusion:

Credit markets often speak before stock markets react. Rising spreads, refinancing pressure, defaults, downgrades, liquidity stress, and private credit risks can all act as early warning signs.

In 2026, global debt levels, private credit growth, geopolitical risks, and refinancing needs make credit-market monitoring especially important. The key lesson for investors is simple: do not only watch market prices; watch the quality of borrowing and lending behind the market.

A healthy investment approach is not built on panic. It is built on awareness, discipline, diversification, and timely review.

Disclaimer: The information provided in this blog is for educational purposes only and should not be considered as financial advice. We recommend consulting a certified financial professional before making any major financial decisions. Omega Financial is not liable for any decisions made based on this material.

Investment in the equity market and securities is subject to market risk. Please read all the scheme-related documents carefully.

Omega Financial is an AMFI-registered mutual fund distributor.